The Opportunity

We have been aware of Titon since the 1990’s. They have a reputable and long-standing brand, good quality products but were previously uninvestable under prior management and had been loss-making since 2022 with the dividend pulled.

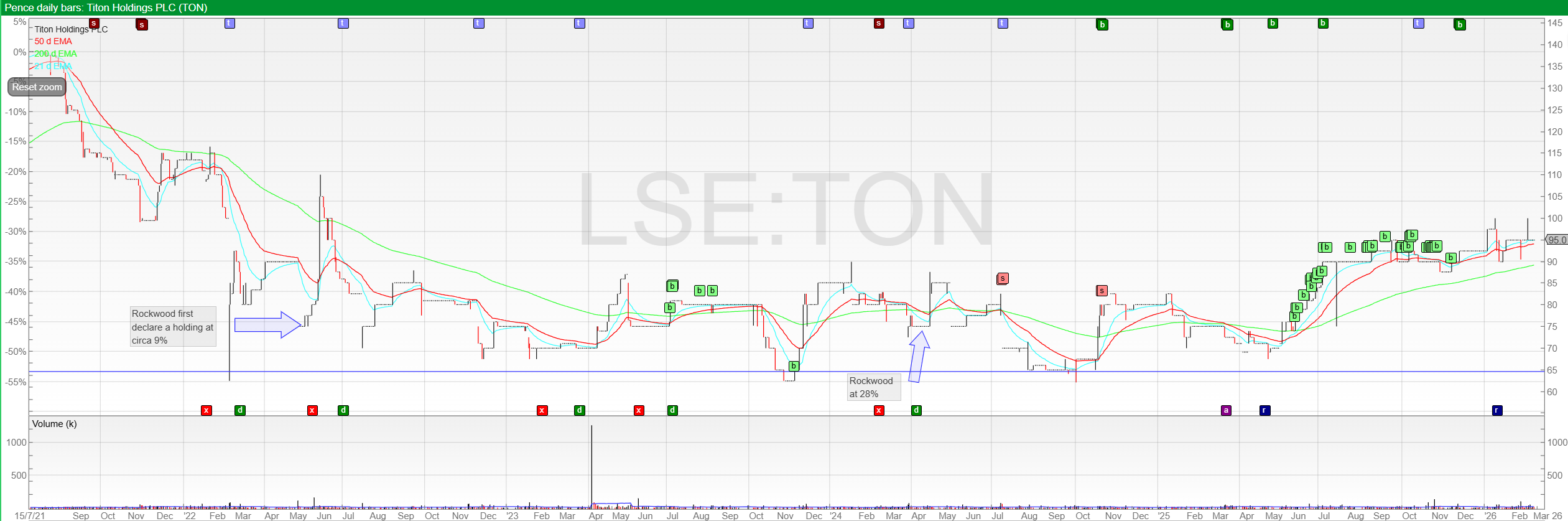

Why we invested

In November 2023, a new CEO was appointed and the previous Executive Chair retired. This was followed in mid-2024 by the founder’s son leaving the Board, and in late 2024 the Group disposed of its loss making Korean venture. The Group was once again investable and had a well-respected new major shareholder in Rockwood Strategic / Harwood Capital in place.

Our Investment Approach

Although we initially started buying the shares in mid-2023, we more actively bought the stock from June 2025, and by November 2025 we owned 3% of the shares outstanding.

Our thesis is that under new management the Group should be able to grow to >£20m of sales and at least £2m operating profit by 2028 and that the current enterprise value of just over £7m (at 95p) is therefore anomalous.

What Happened

In January 2026, the Group reported a return to profitability despite ongoing weakness in their end markets. It’s still early days still in turnaround but we anticipate ongoing operational improvements and anticipate that the Group will likely be acquired by a larger peer. We believe the Group could be worth circa £25m including its valuable freehold properties and hence foresee a >100% return over our holding period.